This week, the total inventory of construction steel continued to decline, with rebar inventory down 4.24% WoW and wire rod inventory down 7.67% WoW. Supply side, pig iron production continued to increase, raw material price pressure began to emerge, steel mill profits contracted, but high supply pressure remained. EAF steel mills faced difficulties in collecting steel scrap and amplified losses, leading some electric furnace mills to shorten operating hours. However, one electric furnace mill resumed production as planned this week, driving up the national operating rate and resulting in a slight increase in overall supply. Demand side, the issuance of domestic special bonds accelerated, the downward trend of real estate data reversed, and steel mills remained in a destocking state, with the overall fundamental imbalance not yet prominent.

This week, total rebar inventory stood at 6.5574 million mt, down 290,300 mt WoW, a decline of 4.24% (previous: -5.79%), and decreased by 1.9784 million mt compared to the same period last year, a decline of 23.18% (previous: -22.64%).

Table 1: Rebar Inventory Overview

Data source: SMM

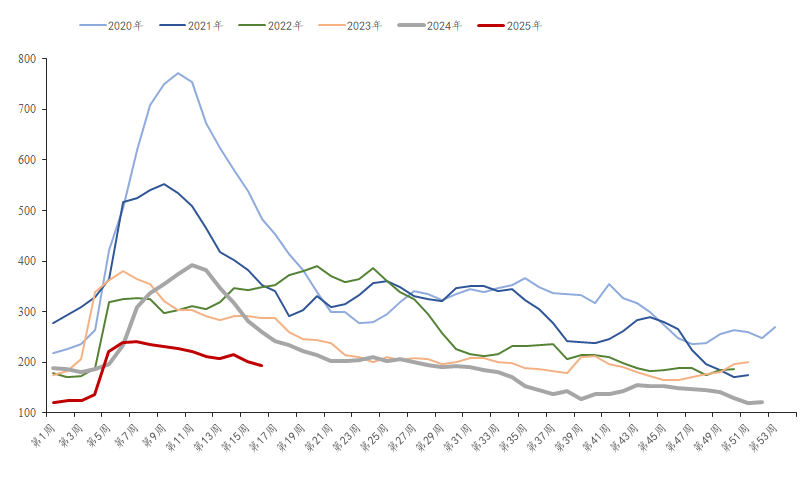

This week, in-plant rebar inventory was 1.9466 million mt, down 68,500 mt WoW, a decline of 3.4% (previous: -6.72%), and decreased by 389,500 mt YoY, a YoY decline of 16.67% (previous: -16.85%). Currently, direct supply from steel mills is good, and in-plant inventory of construction steel continues to decline. However, as previously idled steel mills gradually resume production, the overall supply level has increased, leading to a narrower decline in in-plant inventory this week compared to the previous period.

Chart-1: Rebar In-Plant Inventory Trend, 2020-2025

Data source: SMM

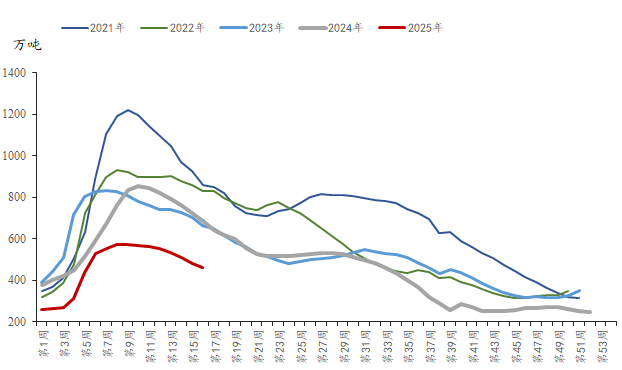

This week, social rebar inventory was 4.6108 million mt, down 221,800 mt WoW, a decline of 4.59% (previous: -5.40%), and decreased by 1.5888 million mt YoY, a YoY decline of 25.63% (previous: -24.82%). Currently, rigid demand continues to recover, and transactions of low-priced resources in the market are moderate. However, due to numerous external uncertainties, overall speculative demand is average. Social inventory continued to decline this week, with the rate of decline slightly narrowing.

Chart-2: Rebar Social Inventory Trend, 2021-2025

Data source: SMM

Overall, the current steel market is influenced by both bullish and bearish factors, with strong market sentiment of wait-and-see. However, as the current inventory level is relatively healthy, the supply-demand imbalance is relatively small. The apparent demand for steel is moderate, and construction steel inventory continues to decline. Considering the upcoming May Day holiday, pre-holiday restocking may release some demand, so steel inventory is expected to continue to decline next week.

![Before the holiday, the black chain is unlikely to see a trend-driven market [SMM Steel Industry Chain Weekly Report].](https://imgqn.smm.cn/usercenter/zUFfM20251217171748.jpg)

![[SMM Chromium Daily Review] Inquiries and Transactions Weakened, Chromium Market Showed Mediocre Performance Before the Holiday](https://imgqn.smm.cn/usercenter/ENDOs20251217171718.jpg)